August 2023 Market Update

A Hilltop Credit Partners Market Report

10 August 2023A Turn In The Inflation Tide?

Recent pull-back in rate expectations provide relief for slowing economy and housing market

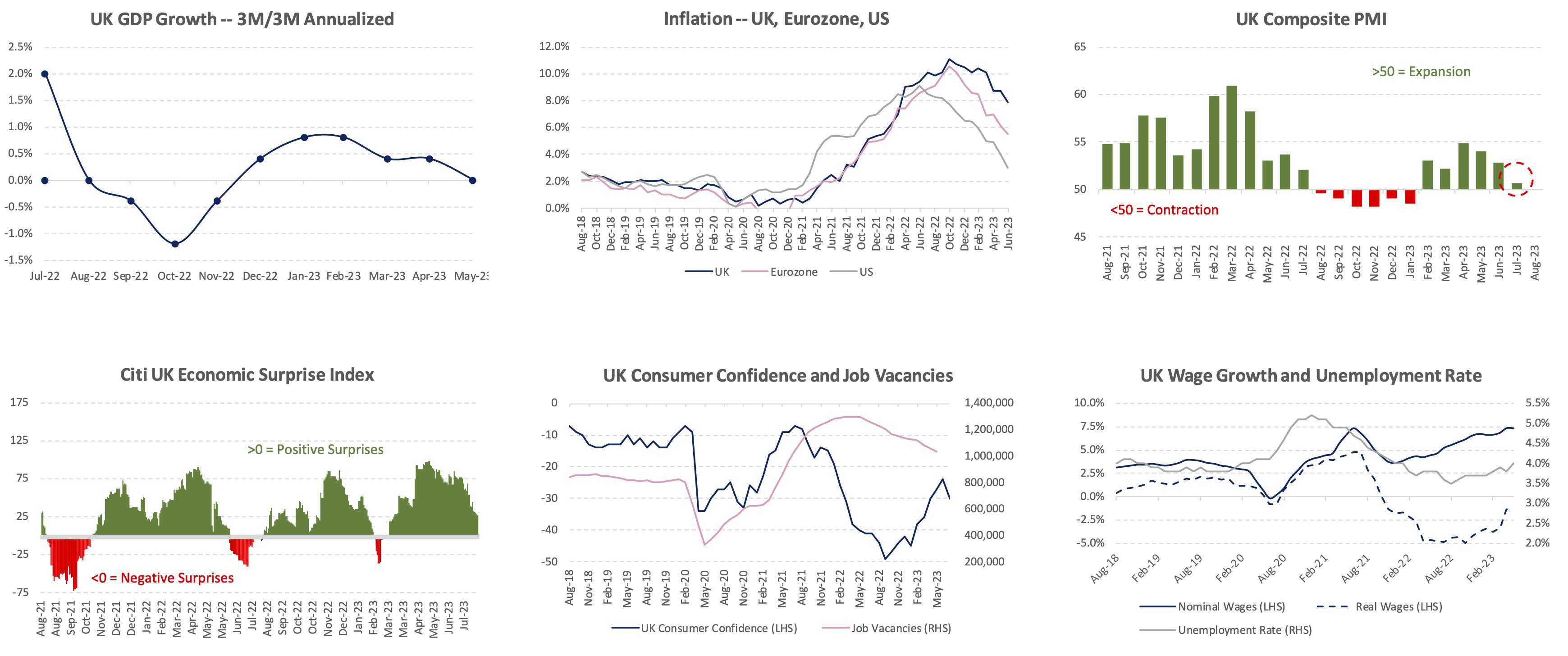

June’s inflation data was a much-needed shot in the arm for the UK economy, housing market and financial markets, coming in below expectations for the first time this year. Inflation fell to a 15-month low of +7.9% y/y, down from +8.7% in May and below expectations of +8.2%. Importantly, core inflation fell for the first time in 5 months.

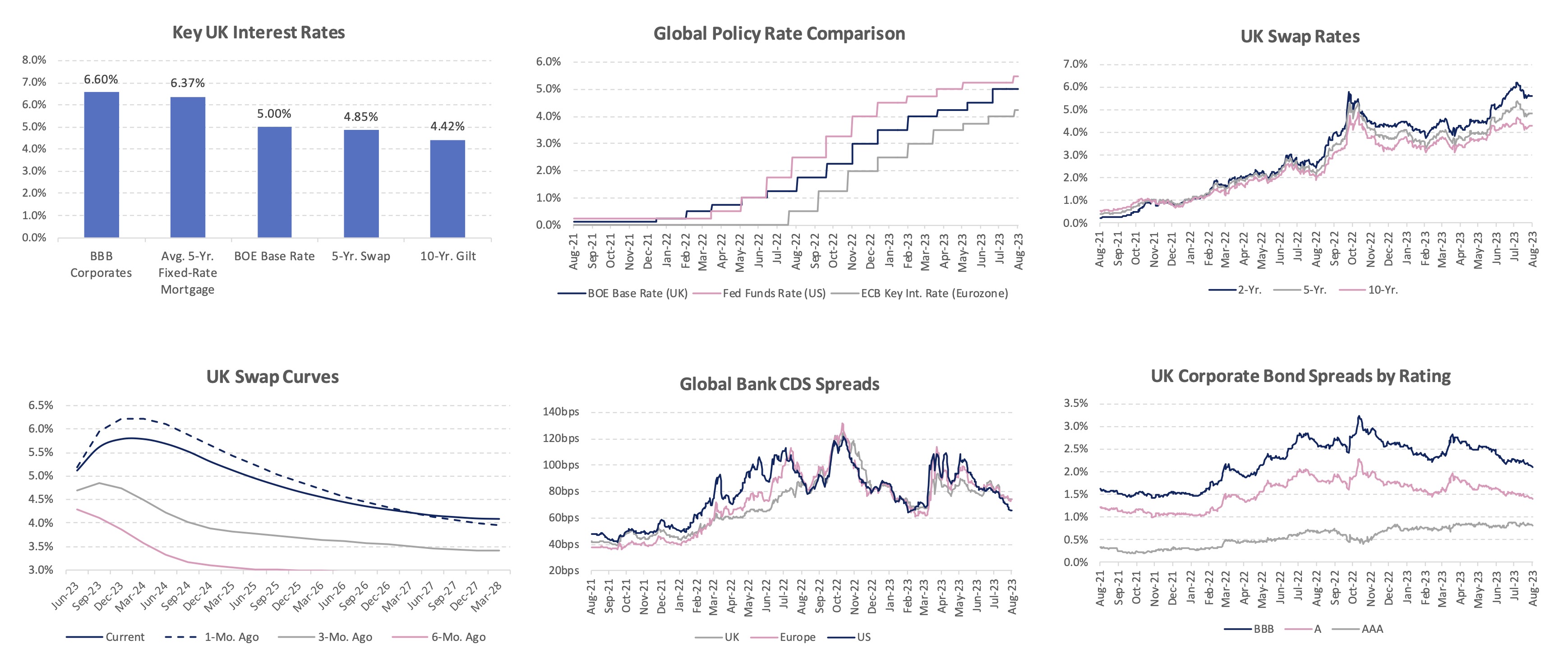

The data has helped to reign in expectations for the future path of interest rates. Over the past 3 months, market expectations for “peak BOE rates” had increased markedly from ~4.75% to ~6.5%, with some market observers predicting rates as high as 7%. Following a round of softer economic, labour market and inflation data over the past several weeks, markets are now pricing in peak rates of ~5.75%, and we believe that over the next quarter, these expectations are likely to fall further.

Why? The Bank of England may well begin to realize (finally) that just as it waited too long to begin raising interest rates, it is now behind the curve again, hiking too aggressively amid mounting evidence that “hot” headline inflation and wage data has been masking an unfolding slowdown as the impact of 13 consecutive rate hikes works its way through the economy.

In the labour market, for instance, payroll data for June clocked in at -9k, significantly weaker than the +23k consensus forecast, while the single-month unemployment rate jumped to 4.3% – the highest level since mid-2021 and in-line with the BOE’s estimate of its “equilibrium rate”. Further, availability of candidates for new jobs rose in June at the at the sharpest rate since the height of the UK’s Covid restrictions in 2020, while job vacancies fell at the sharpest rate since 2009.

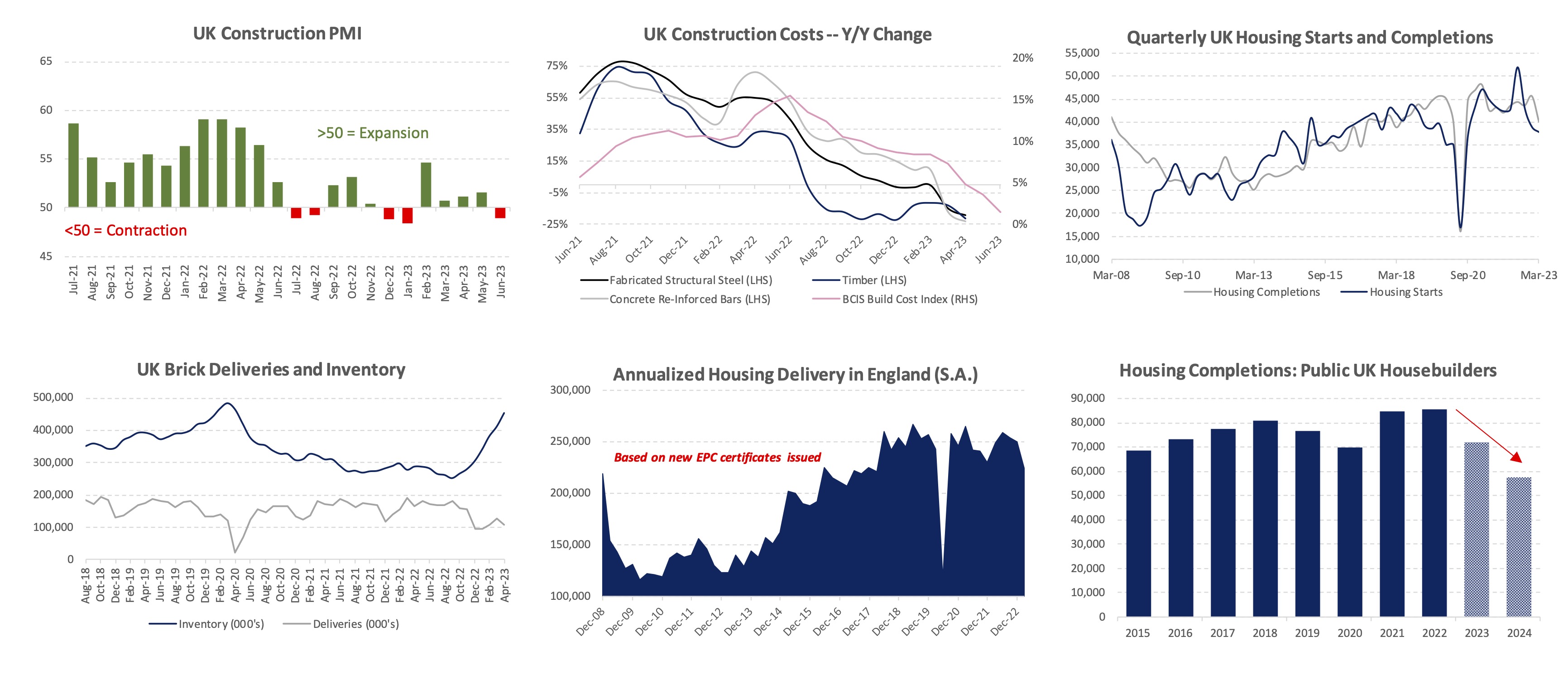

And in the construction sector, prices for key building materials like steel, reinforced concrete, and timber are currently falling at -20% y/y, with BCIS estimating that overall residential build cost inflation slowed from +15.5% y/y a year ago to +1.5% y/y in June, reflecting both a general easing in residential construction activity and gradual re-calibration of supply chains post-pandemic and the disruptions caused by the ongoing Ukraine war. Recent trading updates from large house builders also suggest product availability is improving and that that overall cost inflation will continue to ease through 2023, potentially giving developers more incentive to take new or stalled projects forward.

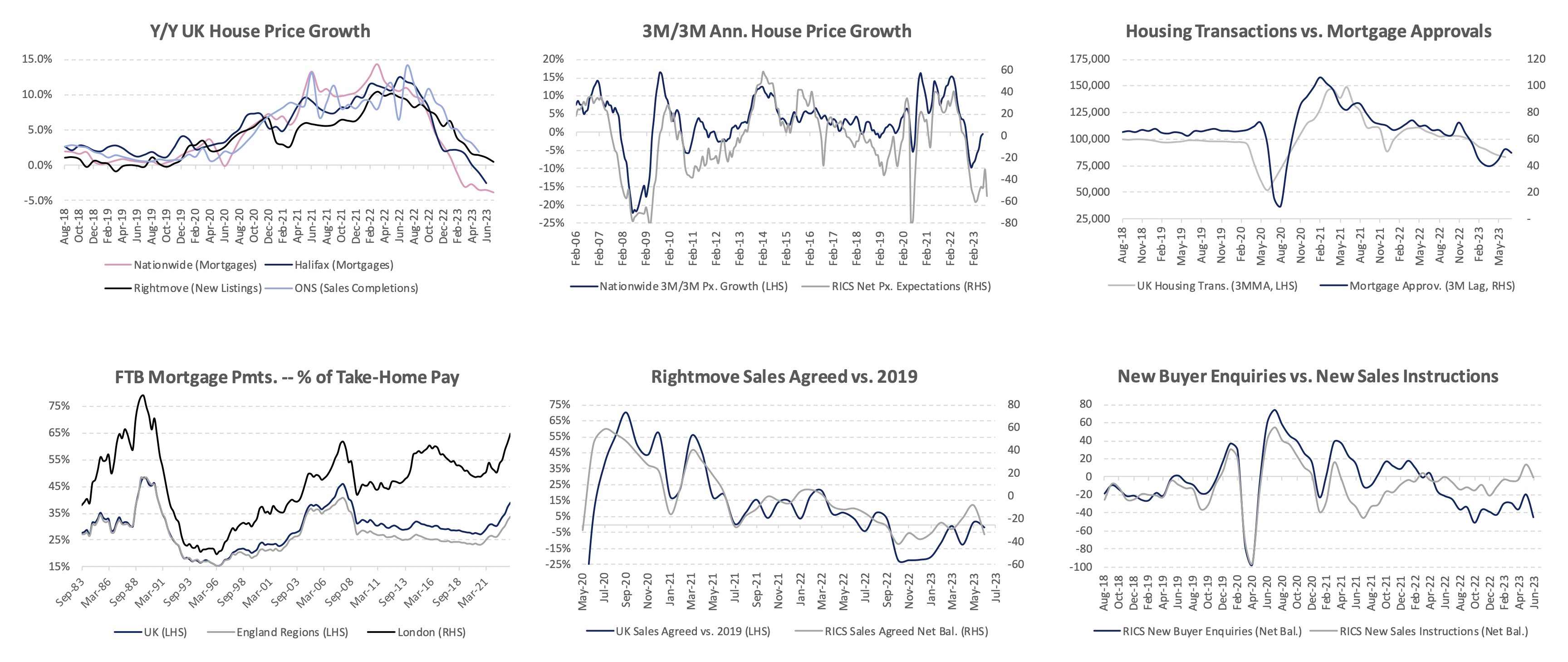

Nonetheless, it is clear that the past year’s aggressive rate hikes are putting downward pressure on housing market activity, with first-time buyer mortgage payments as a percentage of take-home income up from ~28% pre-pandemic to ~40% in Q2 2023. Though UK house prices were basically flat in June and July, putting them down just 4.5% from their Q3 2022 peak, and housing sales agreed across the country continued to rebound to just 2% below 2019 levels, RICS’s June Residential Market Survey registered sharp drops in leading indicators for new buyer enquiries, sales agreed, and house prices, suggesting the market has likely not yet found a bottom.

One ray of light for UK real estate investors and developers: UK rents rose at an exceptionally strong +3.8% in the 3 months to June and are currently +10.4% above year-ago levels and 29.0% above pre-pandemic levels, according to HomeLet. Tenant demand continued to grow in June, according to RICS, while available rental stock also continued to fall, with new landlord instructions (a measure of “rental supply”) plunging to their lowest levels since mid-2020 and reports of a 35% drop in available rental supply vs. 2019 levels.

With rental demand continuing to rise, fuelled in part by intensifying mortgage affordability issues, and available supply continuing to fall against the backdrop of increasingly hostile policies towards private landlords, we believe the path is clear for above-trend rent growth over the next 3-5 years, with a clear opportunity emerging for professional developers and operators of modern, affordable BTR stock.

For the time being, though, housing construction and delivery appears set to slow materially. Brick inventories, inversely related to new housing activity, are up by 58% year-on-year in May. New housing starts have now fallen to their lowest level in over 2 yrs, while guidance and analyst forecasts for the large publicly traded UK house builders suggests new completions could fall 30% by the end of 2024. This would imply industry-wide delivery of sub-200,000 units for the first time in a nearly decade and should be a supportive factor for supply / demand balances in an otherwise challenging market.

UK Macro

June inflation data surprised to the downside for the first time in 2023.

Key Take-Aways:

- UK economic growth remains stagnant, with GDP still 0.5% below pre-Covid levels, though the economy has to date avoided a much-expected recession, helped by significantly lower energy prices and a strong labour market.

- July’s preliminary PMI of 50.7 was softer than expected and the lowest in 6 months; and after rebounding to its highest levels in over a year, consumer confidence took a hit in July, likely in response to recent mortgage rate hikes.

- Inflation has not fallen to the extent seen in the US or Eurozone, driven in part by the ongoing effects of Brexit on the labour market and supply chains, but importantly June inflation came in lower than expected for the first time this year.

- Sharp drops in raw material prices, a slackening labour market, and the lagged effect of 13 rate hikes provide hope that the BOE is confronted with a more benign inflation backdrop in 2H 2023, lowering the chances they will “over-tighten” in the short term and potentially even providing cover for a “pause” over the coming months.

UK Interest Rates

Rate expectations have increased over the past 6 months but are down from recent highs.

Key Take-Aways:

- Stronger-than-expected wage and inflation data have increased market expectations for “peak BOE rates” from ~4.75% to 5.75% over the past 3 months, though this is down from recent highs of ~6.5%, helped by June’s inflation data, which surprised to the downside, with core inflation dropping for the first time in 5 months.

- 5-year swap rates, a key benchmark used in setting mortgage rates, have increased from 2.5% to 4.7% over the past year but are down from their Jul. 7 peak of 5.4%. Over the same period, the average cost of a 5-year fixed rate mortgage has risen from 5% to >6%, but we expect mortgage lenders will reduce rates in light of the recent pull-back in swaps.

- UK corporate bond spreads and global bank CDS spreads have both drifted lower over the past quarter, suggesting investors are relatively calm regarding overall corporate credit risk and stability within the banking system.

UK Housing Market (Sales)

Transaction volumes will remain subdued in 2H’23; prices have likely not yet bottomed.

Key Take-Aways:

- UK house prices are now down ~4.5% from their peak but still up 20% vs. pre-Covid levels. RICS leading indicators suggest prices have not yet bottomed and could fall another 3% or so in Q3.

- Monthly transaction volumes have fallen from ~105,000 in 2022 to ~85,000 in June 2023. We believe Q3 will see a bounce in reported transaction volumes (based on the Q2 uptick in mortgage approvals and sales agreed) before a Q4 roll-over in response to recent increases in mortgage rates.

- Rightmove reports “buyer demand remains resilient, being 3% higher than 2019, with agents reporting that right-priced homes are still attracting motivated buyers due to a shortage of property for sale compared to historic norm.”

- However, mortgage payments as a % of take-home pay for first-time buyers have now risen to 39% -- up from 30% at the beginning of 2022 – which is likely to keep a lid on transaction volumes and prices for the balance of the year.

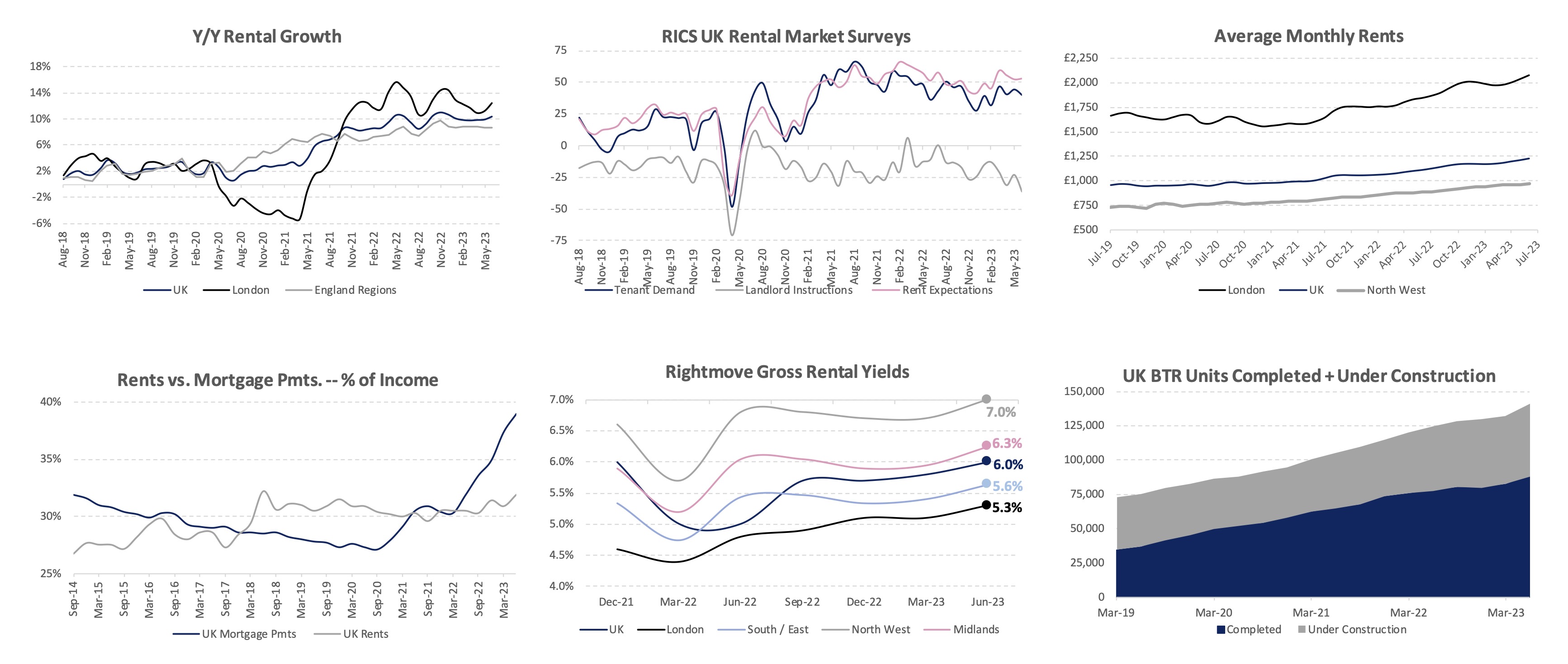

UK Housing Market (Rental)

Rising demand and falling supply is driving record growth in UK rents.

Key Take-Aways:

- UK rent growth remained strong in June at +10.4% y/y. UK rents have now risen by 30% vs. pre-pandemic levels, with avg. London rents having now surpassed the £2,000 / mo. mark for the first time ever. Nationwide gross rental yields hit 6.0% in Q2 2023 – up from 5.0% a year ago, according to Rightmove.

- RICS indicators for tenant demand and rent expectations remained strong in June, and TwentyCi reported continued declines in the number of available UK rental properties, with 241k units available in June – a drop of 35% from 2019 levels. RICS reported that landlord instructions (a measure of supply) fell to 3-year lows.

- Renting has become increasingly affordable vs. buying with a mortgage (32% of average income vs 39%).

- Cumulative BTR delivery stands at 88k units + 54k under construction. This represents just 3% of total PRS stock and is unlikely to make a meaningful dent in solving the acute rental shortage facing the country.

UK Construction / Housebuilding

Construction cost inflation has slowed sharply from 15.5% y/y to 1.5% y/y.

Key Take-Aways:

- The UK Construction PMI for June came in below 50 for the first time in 5 months, signalling contraction in activity. Anecdotally, new brick deliveries are running >20% below “normal levels” while brick inventories are running +58% vs. year-ago levels.

- Housing starts have fallen by 25% from their peak a year ago, while EPC data suggests real-time housing delivery is running at its lowest level since 2017 (excluding the summer 2020 “Covid plunge”),

- Company guidance and analyst forecasts for the “Big 8” publicly traded housebuilders call for a ~30% drop in output from 2022-2024. This implies that total housing delivery could fall to <200,000 units for the first time since 2015.

- Construction cost inflation has ebbed significantly, with prices for key raw materials (e.g., fabricated structural steel, reinforced concrete, timer) down 20% y/y. BCIS estimates UK construction cost inflation has fallen to +1.5% y/y.