UK Housing Market Update - A Market of Cross-Currents

By Tiger Craft, President and Chief Operating Officer of Hilltop Credit Partners

17 November 2023A Market of Cross-Currents

By Tiger Craft, President and Chief Operating Officer of Hilltop Credit Partners

In our previous Market Update, we noted that expectations for peak UK policy interest rates (then at 5.75%) were too high, given the rapid slowdown in the high-frequency labour market and economic data. Since that time, the data has continued to soften, and the BOE has indeed backed off its hawkish stance. Employment contracted in August and September (vs. expectations for >30k job additions) while PMIs dipped below 50, signalling moderate economic contraction after 6 months of growth. This has given the BOE cover to hold rates at its last two meetings, and markets now expect no further tightening with rates beginning to fall again from their current level of 5.25% starting in mid-2024.

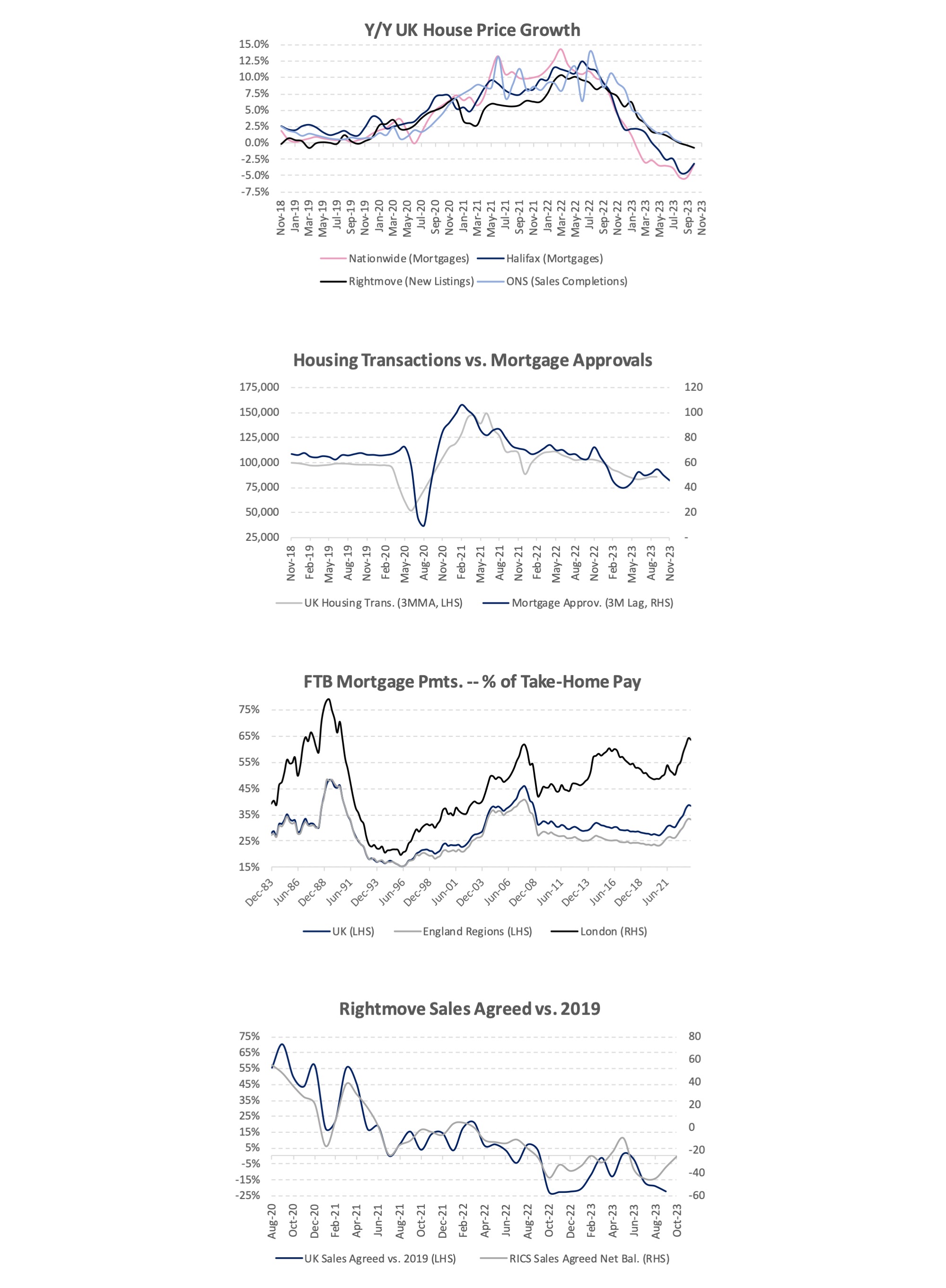

Mortgage buyers have felt some relief with the cost of the average 5-year fixed mortgage falling from ~6.3% at the end of July to ~5.2% today. Nonetheless, with ~1.2 million fixed-rate mortgages rolling off over the next year – 90% of which were priced below 2.5% – the effect of higher mortgage rates will continue to be a drag on sentiment, affordability, and activity levels. The strain can be seen most visibly in the transaction data which remains subdued. Volumes averaged just over 85,000 in Q3, ~15% below historic averages, and leading indicators give little hope of near-term recovery. Mortgage approvals averaged 46,000 in Q3 – roughly 30% below normal levels – while Rightmove reports that “sales agreed” were 17% below normal with more affordable markets (e.g. Scotland, North East) showing more resilience.

While transactions have been weak, house prices have so far been more resilient than expected rising by ~1% in October. Prices are down just -4.5% vs. their 2022 peak. This resilience reflects a combination of limited stock on the market and very few forced sellers, aided by new mortgage regulations which discourage repossessions, healthy levels of borrower equity, and a relatively low unemployment rate. The lack of a “liquidity” crunch – at least so far – differentiates this downturn from previous ones (e.g. 2008 / 1990) when price adjustments were large and swift. That said, in certain UK postcodes where plentiful foreign (e.g. Russian / Middle East) money has driven net yields to unsustainably low levels -- say 2-3% -- developers sitting on over-levered, unsold stock that needs to clear in an investment world of 6% buy-to-let mortgages – may be in for some painful surprises with forced sellers accepting discounts of 25% or more.

It is worth noting that in “real” terms (i.e. adjusted for inflation), house prices across the country have already fallen by ~15% from their peak. A further 5% drop in headline prices over the next year, coupled with 5% inflation, would mean a 25% peak-to-trough drop in real house prices in-line with the pullback seen during the global financial crisis. In short, inflation has already caused a more pronounced downturn in house prices than is readily visible in the headline data.

“We see affordable build-to-rent presenting a significant opportunity for both long-term equity and lenders in a challenging market.”

Paul Oberschneider, Founder and Chief Executive Officer of Hilltop Credit Partners

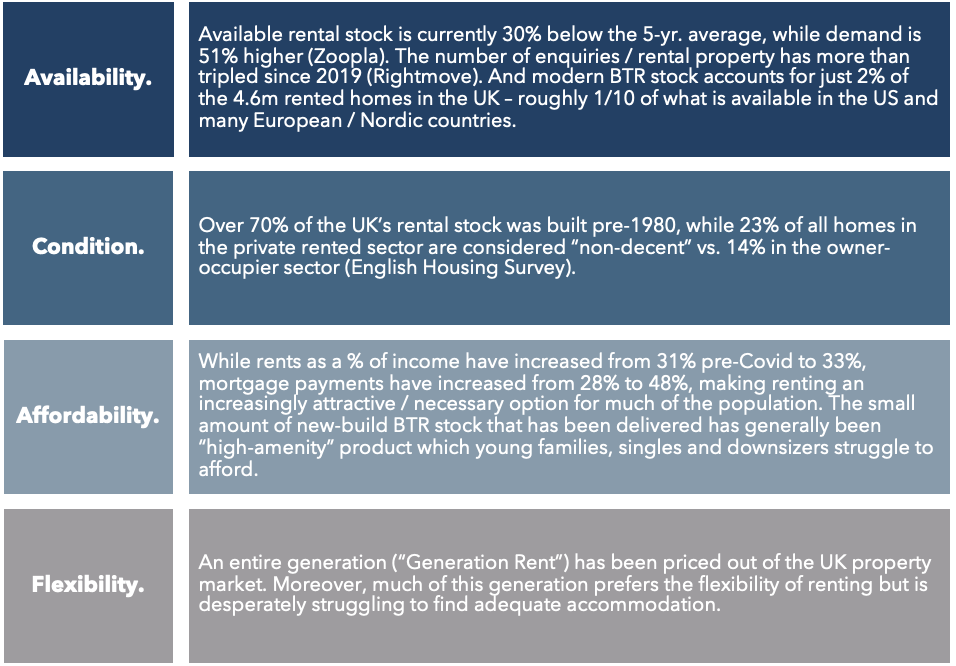

Strong growth in rents continues to be another factor underpinning residential asset values. UK rents rose +10% y/y in September and are now +34% vs. pre-pandemic levels. In our view, there are 4 key drivers of the extremely tight supply / demand balances underpinning the UK rental market:

We consider the huge contraction in rental supply coupled with strong secular demand growth to be a huge opportunity for an affordable “build, aggregate and scale” strategy that supports smaller developers to deliver a new BTR product that we believe is in high demand across numerous regions in the UK.

Speaking of the need for newbuild rental stock . . . house building activity had been contracting for 11 straight months according to S&P’s construction PMI, and the latest completions data shows output at the lowest level since 2020. We believe significantly lower levels of completions are likely over the coming year, exacerbating what is already a structurally under-supplied market.

The good news for house builders is that prices for key construction materials are now falling at over 25% y/y, improving development economics for sensible projects. And with a General Election looming, both parties are mulling various options to support struggling developers, house buyers, and renters.

UK Macro

The UK entered a shallow recession in late Q3; inflation to drop towards 4% in coming months.

Key Take-Aways:

- The UK appears to have entered a shallow recession in late Q3, following 6 months of expansion. October’s Composite PMI of 48.6 is consistent with annualized GDP declines of roughly -0.5%. Economic data began surprising to the downside in late October, following 6-7 months of positive surprises.

- Headline inflation has cooled from +11.1% to +6.7% over the past year, with leading indicators pointing to a drop towards ~4% in the near-term. This indicates that the BOE is almost certainly done tightening, with its next move likely to be a rate cut.

- The unemployment rate has hit a cycle high of 4.3% and is likely headed towards 5% -- levels not seen since the 2021 Covid lockdowns. Private jobs contracted by 12,000 in September + October (vs. est. of +33,000 job additions).

- Wage growth of +7.8% y/y is outstripping inflation for the first time in 2 yrs. but rising unemployment and falling job vacancies will put downward pressure on wage growth over the coming 12 months.

UK Interest Rates

The BOE is likely done hiking; rates now expected to fall to 4.5% by year-end 2024.

Key Take-Aways:

- The BOE has raised its base rate has from 0.1% in December 2021 to 5.25% but has held rates steady in its past 2 meetings.

- Interest rate markets now believe that the BOE is done with its tightening cycle, with rate cuts beginning in mid-2024, Policy rates expected to fall from current level of 5.25% to 4.5% by year-end 2024.

- This is a welcome development for the UK economy and housing markets. In mid-July, markets had been pricing in BOE rates rising to ~6.5%, with some forecasters suggesting rates as high as 7% would be necessary to tame inflation.

- Softer inflation data and a more dovish BOE have driven 5-yr. mortgage rates from ~6.4% to ~5.4% over the past few months, though 1.2m fixed-rate mortgages will roll to significantly higher rates in the coming year.

- Global bank CDS spreads and corporate bond spreads have been widening since the beginning of September, suggesting growing concern over defaults, but remain below the panic levels seen in March.

UK Housing Market (Sales)

Transaction volumes are depressed; prices have been slower to adjust than in previous cycles.

Key Take-Aways:

- UK house prices rose unexpectedly by +0.9% in October and are now down just -4.5% vs. their 2022 peak and +19.8% vs. pre-Covid levels. The “real” (inflation-adjusted) decline has been significantly higher at -15% (vs. -25% during the GFC).

- Limited availability, a lack of forced sellers, and the prevalence of fixed-priced mortgages (now 80% of the market), is preventing the rapid closing of bid/offer spreads in the market, though this may change as unemployment rises and 1.2m mortgages re-set to higher rates in the coming year.

- RICS’ leading indicator for house prices suggests further declines are likely. A further 5% drop, coupled with 5% inflation, would put “real house prices” down -25% peak-to-trough by the end of 2024.

- Monthly transaction volumes were just over 85,000 in Sept. -- ~15% below pre-pandemic average levels. Mortgage approvals of 43,000 were down 30% vs. pre-pandemic levels and suggest subdued levels of transaction activity in the coming quarters.

UK Housing Market (Rental)

Rents continue to set new highs, with demand 50% above historic levels and supply 30% below.

Key Take-Aways:

- UK rents continue to set new records -- +10% y/y in September and +34% vs. pre-pandemic levels. London is currently showing the strongest rent growth (+12%), with the South West showing the weakest (+5%).

- Rents as a % of income have reached 10-year highs of 33% but remain below mortgage payments of 38%.

- Supply has improved marginally in recent months but remains 30% below the 5-year avg., with demand 50% above, according to studied Zoopla data.

- RICS’s September survey calls for 5-yr. avg. rent growth of ~5.5% -- close to the highest on record.

- Nationwide gross rental yields have now increased to 6.4%, according to Rightmove, this is up from 5.7% a year ago, with the highest yields in the North West (7.2%) and the lowest in Greater London (5.4%).

UK Construction / Housebuilding

Housing completions continue to fall, exacerbating medium-term supply challenges.

Key Take-Aways:

- UK construction activity is contracting at the second fastest rate since May 2020, driven by an 11th consecutive monthly decline in housebuilding according to October’s PMI data.

- Counterintuitively, housing starts rose by 75% in Q2 (the most recent period for which data is available). This was driven entirely by a rush to start projects before a June deadline requiring new homes to produce 30% less carbon emissions.

- Completions fell to their lowest level since Q1 2020 and could fall by another 30% by the end of 2024.

- Key construction material prices continue to fall by >25% y/y, and BCIS estimates that overall build cost inflation is now up just +2.5% y/y, providing a much more stable backdrop against which to underwrite development budgets.