The opportunity for a credit reset, revisiting last years predictions - Did we get it right?

We first published the below article in June 2022, and it is still very relevant today. Read through our market predictions and the opportunities we identified to see how our analytics shape what we do today.

23 May 2023We have been expressing a cautious view on the shifting macro environment for quite some time. We don’t cry wolf all the time, but when we do we hope people listen.

I’d like to think we’re pretty good at connecting the dots, and having been through multiple market cycles helps. But don’t just take our word for it. Read the below article we published in June 2022; it highlighted some of the economic issues we saw unfolding, including the opportunity for a "credit reset", and is still very relevant today. The next set of dots we are connecting is how we can effectively deliver funding for the affordable multi-family and single-family rental sectors - both rapidly growing but still nascent asset classes in the UK.

Market Tops and Opportunity - June 2022

An economics professor of mine once aptly said that markets turn when the rubber band can no longer be stretched and that usually something out of the blue will trigger a sentiment change.

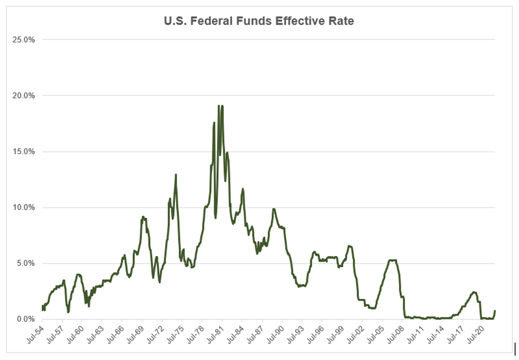

In 1972 the Dow Jones crossed the 1,000 milestone for the first time. Ten years later, the market bottom business headline for all those that can remember was "Equities Are Dead". Interest rates were between 7-11% hitting a high of nearly 20% in 1979. I think it's fair to say 1982 was the beginning of the bull market we have all grown up with; a market which has fuelled asset price growth across all sectors and most geographies. Looking at the chart it's easy to see the correlation. If you just steered straight, and avoided being too clever, and rode the liquidity wave that followed, you probably did pretty well and might even have come to believe how smart you are.

So now what? Brexit gone wrong, Covid 19, a government without reliable leadership, the war in Ukraine, supply chain issues, all have contributed to an inflationary aftermath of a dog's breakfast. I think it's fair to say the salad days are over and we are entering into a period of time most have not been exposed to. Strap in because the world is changing.

What About Residential Real Estate?

Not all asset classes are created equal. That said, both the rising cost of capital and a slowdown from banks and Private Equity into new ventures will have a pronounced effect on residential asset values and project velocity and GDVs; probably not a bad thing to be honest.

For the last several years, we witnessed a mad rush of capital both credit and equity to the bottom of deals, making pricing and returns look extremely low given the bucket of variables that can always go wrong even in a perfect world. But when borrowing costs are near zero, any positive leverage return seemed acceptable - except when the game changes - and that's exactly where we are today. The game is changing.

The good news is that the overall system will prevent massive downward pressure on residential assets; constrained planning, lack of completions in the last two years, and reflex-like shifts from one strategy to another, has not kept pace with the cumulative demand for housing in the UK and Europe. To date, the recent rate increases we are seeing are having a more psychological effect on purchase decisions than a real impact, sales velocity aside.

The bad news is that many development projects will need resetting; borrowers and capital will need repricing and new projects will need to reflect affordability more adequately. No longer can we expect rising GDVs to bail us out, rising build costs and chasing deals will slow down to a snail's pace in my opinion. The days of tripping over ourselves are gone.

What We Are Seeing

As credit investment managers that lend to residential, we are sensitive to all the above issues, and have the benefit of our own growing loan book to give us hints of what the future looks like. Couple that with decades of on-the-ground development experience and having weathered several market disruptions and liquidity lock-ups, we are pretty familiar with what many borrowers will face.

The simple truth is most projects that went into the ground a year/two years ago will have struggled with a host of inflationary and supply chain disruptions. There isn't a loan book in the market that will not have these issues, despite what is being messaged into the market. Add on top of that sales delays and uncertainty, and the fact that most Tier 2/3 contractors cannot make good on contracts creates an avalanche of problems coming onto the horizon.

Stabilisation and Support Finance

With borrowers and bankers looking at their watches in a race for time, Hilltop is taking steps to meet with and find recap solutions to projects that are near completion or need to replace existing contractors in order to finish. The real issue is that historically most lenders shy away from half-finished projects with complications. This is where our experience and network of capital and resources can come into play.

If any of this resonates with you or the projects you are involved in, we'd love to chat.

Hilltop Credit Partners is a real estate credit investment manager that through managed funds and separate accounts provides financing solutions.

You can read the original version by clicking here