UK Economic and Housing Market Update - Q1 2023

UK house prices fell by -0.5% in February 2023 according to mortgage lender Nationwide, marking a sixth consecutive month of declines.

Market update

UK house prices fell by -0.5% in February 2023 according to mortgage lender Nationwide, marking a sixth consecutive month of declines. Prices are down 3.7% from their August peak but still 20% above pre- pandemic levels. The double whammy of rising house prices and rising mortgage costs has stretched affordability, with monthly mortgage payments for first-time buyers now taking up ~40% of after-tax income – below “pre-crash” levels seen in 2007 and 1989 (>45%), but still high relative to historical averages (~30%). While solid gains in nominal incomes (currently running +6-7% y/y), combined with softer house prices and falling mortgage rates, will work to improve affordability over time, we believe that house prices will likely drift lower in the near term as the full effect of mortgage re-pricing works through the system.

The Nationwide data was released the same day the Bank of England announced that mortgage approvals for new home purchases remained at depressed levels of ~40,000 in January – down 40% vs. pre-mini- budget levels seen this past summer, still reflecting a tumultuous Q4 during which mortgage lenders hiked rates rapidly while withdrawing hundreds of products from the market.

The data suggests that monthly UK housing transactions, which have been hovering around long-term averages of ~100,000, may slump to ~70,000 in the coming months – levels not seen since the summer 2020 market shutdown. We expect, however, that 2023’s more accommodative mortgage market (from both a pricing and availability standpoint) will drive transaction levels back to “normal” levels by mid-year.

On a more positive note, the UK economy has seen a few unexpected signs of improvement recently, with falling energy prices and interest rates driving better-than-expected consumer and business sentiment. UK wholesale gas prices have collapsed 50% since mid-December and 75% since their peak last summer, while expectations for peak BOE policy rates have retreated by nearly 30% from their post-mini-budget highs of ~6.5% to ~4.5% in late Feb. Consumer confidence, while still depressed, unexpectedly rose to its highest level in nearly a year in February, while the preliminary reading of S&P’s Purchasing Managers' Index (PMI) exceeded all analyst forecasts, jumping to 53.0 in February from 48.5 in January, suggesting that UK business activity returned to growth in Feb. after 6 months of decline. As a result, HSBC’s economics team believes “it is now plausible that there is no recession at all.”

Housing market sentiment appears to have benefited at least somewhat from this improved macro backdrop. Rightmove reports an increasing number of potential buyers returning to the market in February, with the market starting 2023 “much better than expected.” The UK’s largest online real estate portal reported that the number of people contacting agents was up by 11% in the second and third week of February compared with the same period in 2019 and that the number of sales agreed continues to rebound -- now just 11% down on 2019 levels, vs. 15% down at the start of the year, and 30% down in the aftermath of the mini-budget.

Meanwhile, UK rents continued to grow at a record pace of ~10% y/y in February according to HomeLet, with demand being driven by demographic factors and increasing cost of home ownership, and supply contracting as new BTR delivery fails to offset the continued exodus of private landlords who have faced numerous challenges, including rising buy-to-let mortgage costs, elimination of tax deductions on interest, and new requirements around EPC certification. Knight Frank notes that the prospect for further reform impacting the buy-to-let sector could reduce private landlord numbers even further.

RICS’s January Residential Market Survey recorded a near 20-year high in the net balance of market participants expecting further rent increases over the next 3 months, while expectations for annual rent growth over the next 5 years also sit near 20-year highs of c. 5% / yr. 91% of RICS survey respondents believed that BTR would be unable to fill the shortfall in supply across the lettings market to a significant extent.

And speaking of supply shortfalls, a new report from the Home Builders Federation suggests that changes by ministers to England’s planning framework and the impact of government environmental rules could result in housing delivery falling to the lowest level in 80 years, with net housing additions dropping from 233,000 last year to <120,000 in the coming years – well below the government’s supposed 300,000 / year target.

Regardless of the economic climate, this is likely to keep supply/demand balances tight, preserving the scarcity value of UK Residential as an asset class over time.

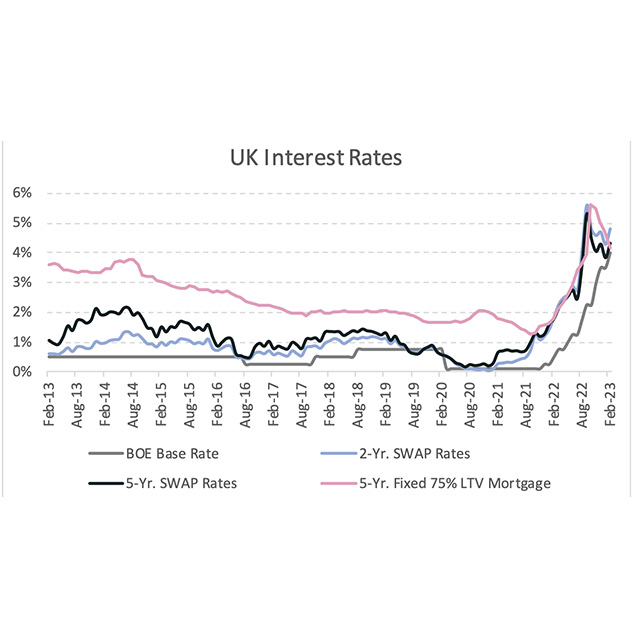

Figure 1: UK Interest Rates

BOE policy rates have risen from 0.25% at the beginning of 2022 to 4.00% at the end of Feb. Market expectations are now for rates to peak ~4.5%, down ~6.5% in late Q3. Rates on a 75%-LTV, 5-year fixed-rate mortgage, which briefly topped 6% late last year, have fallen to just above 4% today.

Source: Bank of England (base rate and mortgage rates through Jan. 2023); Nationwide (Feb. 2023 mortgage rates; uk.investing.com (swap rates).

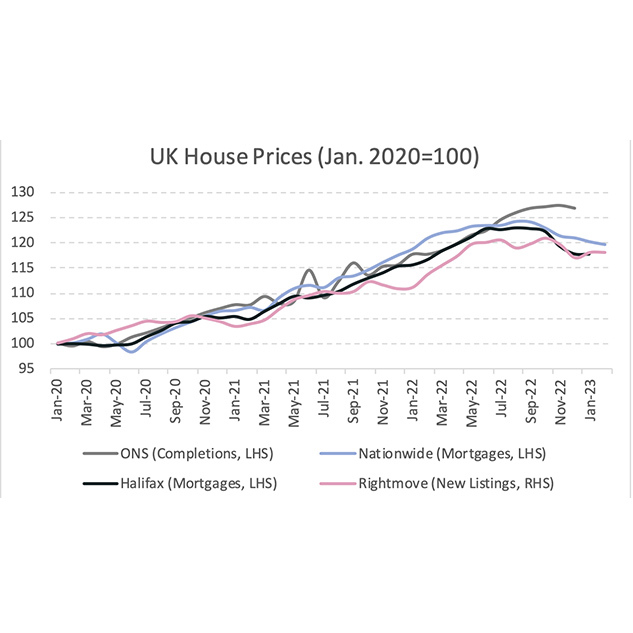

Figure 2: UK House Prices

Nationwide’s seasonally adjusted house price index showed its sixth straight monthly decline, representing a -3.7% decline since the August 2022 peak and a +19.6% gain since the beginning of 2020. Leading-edge asking prices from Rightmove have actually moved slightly higher (+0.9%) over the past two months, suggesting some stability may be returning to the market.

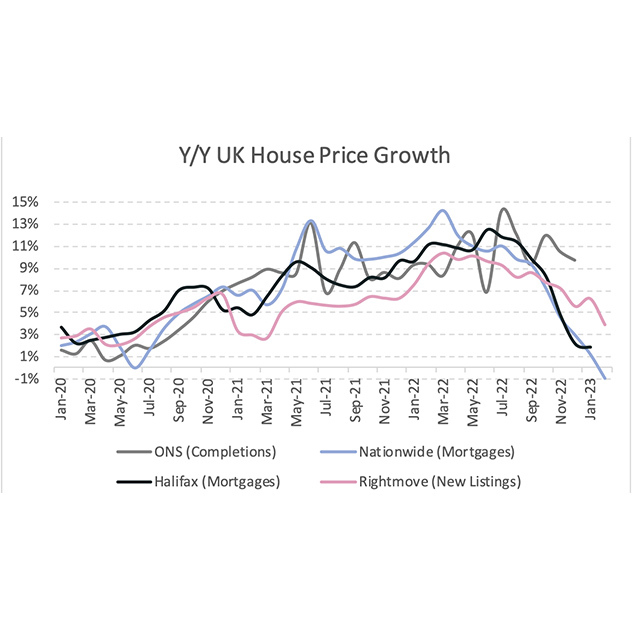

Figure 3: Y/Y UK House Price Growth

House prices are now down running down -1.0% y/y according to Nationwide – the first y/y decline since June 2020 (-0.1%) and the largest y/y decline since Nov. 2012 (-1.2%). Rightmove’s house price index (the only other source for which Feb. data is available) shows prices running +3.9%, but we would note that these are asking prices rather than achieved prices.

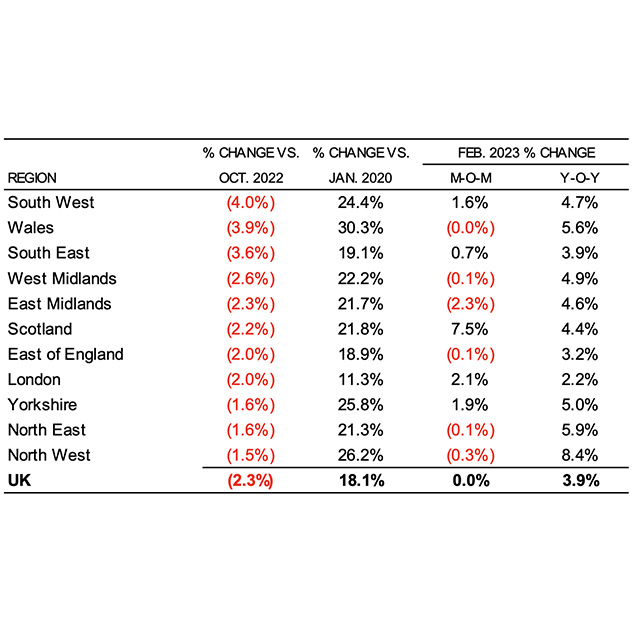

Figure 4: UK Asking Price Growth by Region (Rightmove)

According to Rightmove, asking prices have fallen most over the past 4 months in the South West (-4.0%) and Wales (-3.9%), while the North West (- 1.5%) has fared the best, likely driven in part by the higher rental yields on offer and the strong current demand for rental stock in a severely supplied rental market.

Figure 5: UK Housing Transactions vs. Mortgage Approvals

January 2023 data from HMRC showed a relatively healthy 96,650 housing transactions down -10.6% y/y but just -2.9% below the 10-year average. However, given the post-mini-budget collapse in mortgage approvals to 10-year (ex-Covid) lows, we expect transaction figures to fall to ~65,000 – 70,000 in the Feb/March data before gradually recovering through the second quarter.

Source: HMRC (housing transactions); Bank of England (mortgage approvals).

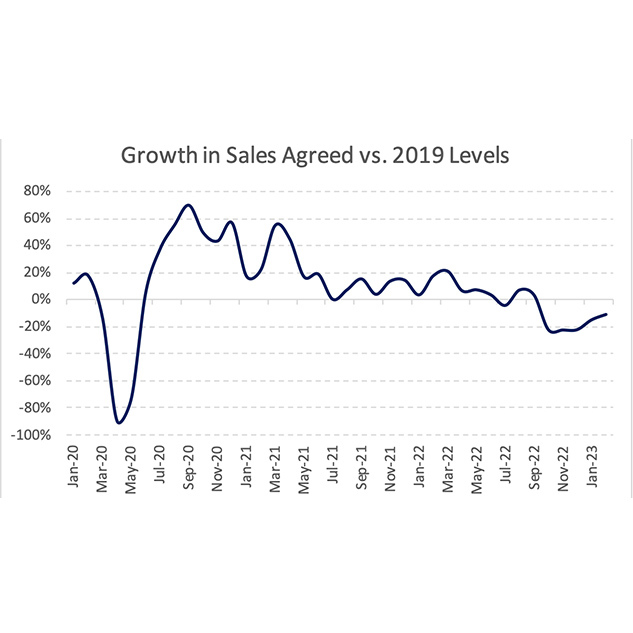

Figure 6: UK Sales Agreed (Rightmove)

We track trends in sales agreed as a leading indicator four housing market activity. Sales agreed have doubled from the extremely depressed levels seen in December and are now down just -11% vs. 2019 levels vs. -20% in December and -30% in the weeks following the mini budget, supporting our view that mortgage approvals and housing transactions should recover towards more levels as Q2 unfolds.

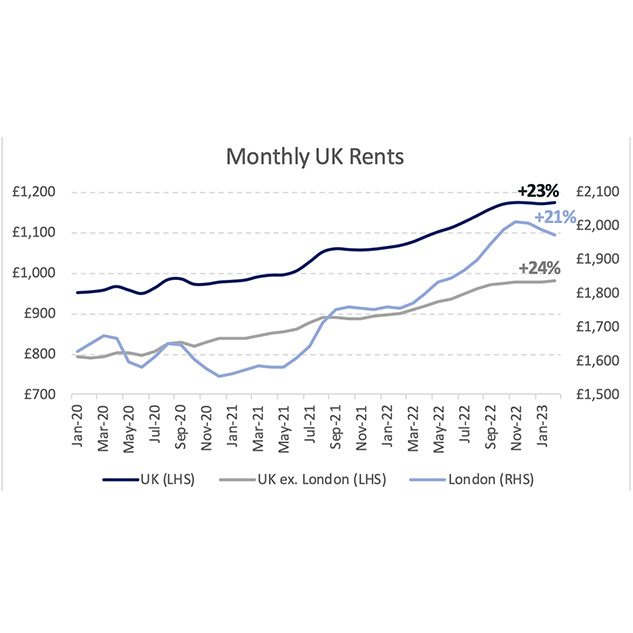

Figure 7: UK Rents

Rents across the UK have risen by over 20% over the past 3 years, driven by strong secular demand trends, rising house prices, shrinking supply of available rental stock as regulatory and tax drive private landlords out of the market, and more recently increasing mortgage costs. The London market was hit hardest by Covid lockdowns but has rebounded sharply.

Source: HomeLet

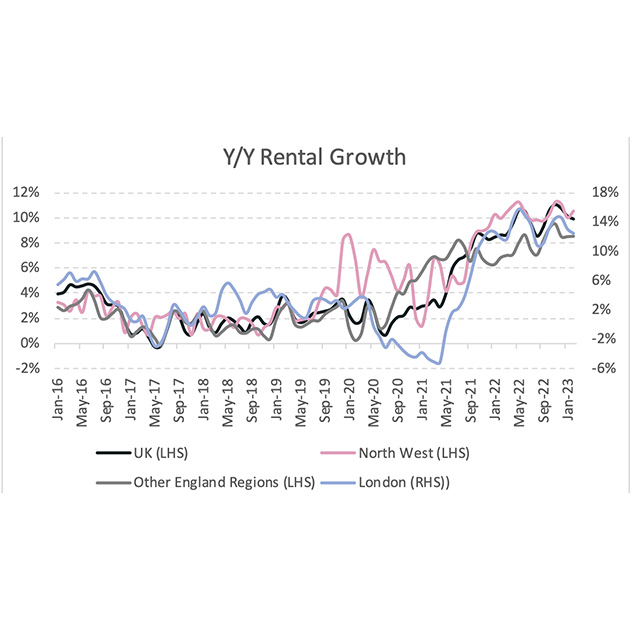

Figure 8: UK Rental Growth

Rents across the UK grew at +9.9% y/y in February, with the strongest growth witnessed in the North West of England, driven by the “Northern Powerhouse” markets of Manchester and Leeds.

Source: HomeLet

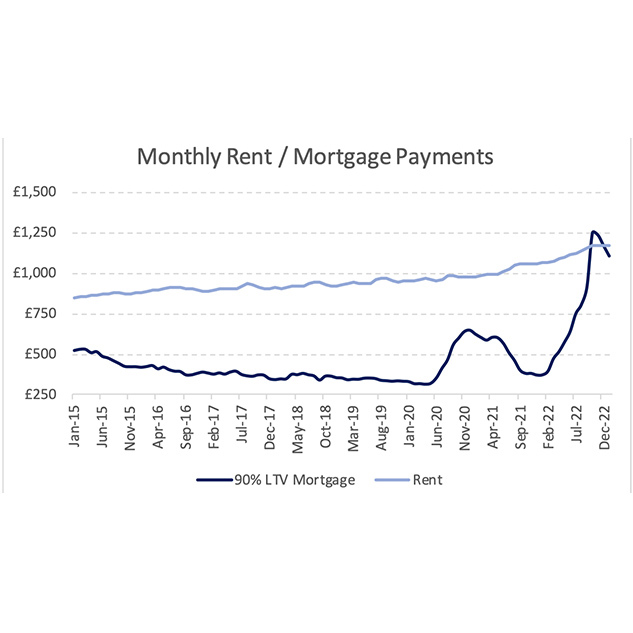

Figure 9: Rental vs. Mortgage Affordability

From 2015-2021, it was ~50% cheaper for a first-time buyer to service a 90% LTV mortgage than it was to rent. Despite significant increases in rents over the past few years, it is now roughly as expensive to buy as it is to rent, while finding a £25,000 deposit is a struggle for many first-time buyers. This has been one of several factors driving rental demand over the past 12 months.

Source: Monthly mortgage payments based on the cost of a 2-year fixed 90% LTV mortgage per BOE data and Nationwide average house prices. Average monthly rents are from HomeLet.